- Admin

- August 13, 2025

- 11 months ago

- No Comments

Introduction

In Kenya’s vibrant agricultural sector, livestock farming is a cornerstone of economic activity and rural livelihoods. However, a significant challenge faced by many farmers, particularly smallholders, is the financial barrier to accessing timely and essential veterinary services. This often leads to delayed treatment, worsening animal health, and ultimately, reduced productivity and income for farmers. For veterinary practices, this translates into missed opportunities for growth and impact.Therefore, the strategic extension of credit to clients emerges not as a compassionate gesture and a powerful business balance for practitioners. It is a mechanism that can enhance client loyalty, broaden service accessibility, and contribute to the long-term sustainability and profitability of a veterinary practice.

When we discuss ‘credit’ within the veterinary domain, we are referring to the practice of providing veterinary services, medications, or products to clients with an agreement to pay on a later date. From our studies in the Kenyan environment, it shows that credit ranges from informal, direct payment plans negotiated between the veterinarian and the client, to more formalized arrangements involving third-party financial institutions or even specialized microcredit schemes tailored for agricultural communities Eg. Milk and tea societies.

Farmers often find their animals in distress and need Veterinary services for life saving procedures. An animal in distress cannot wait for a farmer to secure funds; immediate intervention is often critical for survival and recovery.

Therefore, the provision of credit in this sector demands a delicate balance: addressing the immediate need for care while wisely managing the financial realities of both the veterinary practice and the client. For veterinarians operating in Kenya, knowing when to extend credit—and when to hold back—can be the difference between a thriving business that pays you and one that struggles to survive.

Important terms to note:

- Credit Limit: it’s the ceiling you set for how much treatment, medication, or other services a client can receive on credit before they must pay part—or all—of their balance.

- Repayment Period: Duration before sending the first reminder to the client (e.g., 3 days, 7 days,, aligned with farmer income cycles eg. milk payouts)

- Payment Schedule: Frequency and amount to pay with clear due dates.

- Invoice – The main role of an invoice in credit management is to formally document the amount a customer owes and the payment terms, serving as a clear request for payment.

- Consequences of Non-Payment:What steps to be taken if payment is not made

Why give credit?

Mwangi is a dairy farmer in a rural area near Eldoret. His livelihood depends on the health and productivity of his cows, which provide milk to sell at the local dairy cooperative. Every two weeks the cooperative pays Mwangi for milk supplied during the duration.

When one of his cows falls sick, immediate veterinary care is critical to save the animal and avoid losses.

Mwangi does not always have cash on hand, especially before the milk payments arrive. But because of the trust built over years, his vet, Hesborn, offers him credit. Hesborn treats the cows and sends Mwangi an invoice by SMS, showing the services provided and the amount owed.

Mwangi carefully tracks his expenses and repays Hesborn every two weeks after receiving his milk payment. This credit arrangement helps Mwangi keep his cows healthy without the stress of upfront payment, and it helps Hesborn maintain a steady client relationship and business income.

However, this kind of trust and credit works because Hesborn documents balances left and Mwangi is a responsible client with a predictable income and good repayment history.

When to Offer Credit?

Not every client is like Mwangi here. So let’s get into when it would not be wise to give credit any time a client asks for it.

Here are 5 examples of when to offer credit:

- Emergencies and Life-Saving Interventions: if an animal’s life can be saved and the client has no money at that moment, a vet may decide to save the animal and collect later.

- High-Value Procedures or Treatments: For costly but essential procedures—such as surgeries or long-term treatments—offering credit allows clients to pay in installments, making care more affordable and accessible.

- Predictable Income Cycles: If the farmer has a consistent income. A good example is the milk payment cycles when a farmer is more liquid.

- Loyal clients: Clients who consistently choose your business and maintain a strong relationship with you.

- Disaster or Crisis Situations: Offering temporary credit to your clients during droughts, floods, or disease outbreaks shows support and helps strengthen long-term client relationships.

Who Should You Give Credit To?

While the benefits of extending credit are compelling, it is equally important for veterinarians to determine who to give credit. Giving every client credit leads to substantial financial setbacks for the practice. It is therefore important to do a systemic assessment on your clients to ensure long-term sustainability of the relationship between the vet and the client. This process necessitates the evaluation of a client’s trustworthiness, their demonstrated capacity to repay, and the fundamental nature of their farming operation.

- Existing, Reliable Clients:Farmers or pet owners who pay up when they have cash and don’t lean too much on credit.

- Clients who have predictable sources of income

How Vet Mkononi Helps You Track Unpaid Balances

With the information above, we see that credit is a powerful tool if used correctly. If Hesborn denies Mwangi credit, he risks losing a loyal customer. But if he doesn’t track Mwangi’s balances properly, he risks losing a lot of money—something that could even threaten his entire practice.

Vet Mkononi is a tool tailored for such a situation because it helps vets like Hesborn:

- Easily track client balances: Vet mkononi records cost of service provided and the amount paid by the farmer. This is sent to the client as an sms invoice to ensure the farmer has a copy of the invoice.

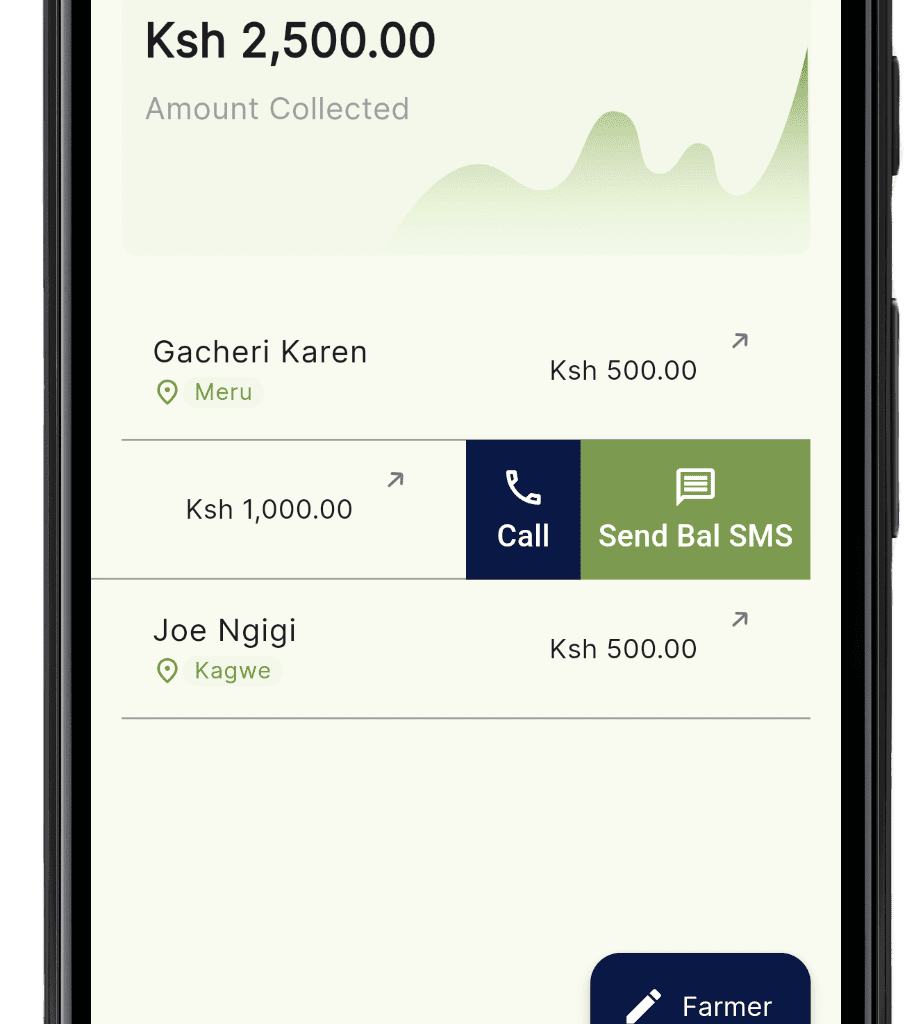

- Manage credit terms: Client balances are always displayed on the app’s homepage, showing you exactly who owes you and how much. With this information, you can easily decide whether to offer a customer another service or wait until they clear their existing debt.

- Send timely payment reminders. From the homepage, you can quickly send a payment reminder by swiping left on the client’s name to reveal a green clickable button labeled: “Send Bal SMS.” The client will automatically receive an sms reminder.

- Accurate reports: In the Reports tab, you can easily view your practice’s unpaid revenue at a glance. Having clear insight into outstanding payments empowers you to make informed decisions about offering credit to your clients, helping you manage your cash flow effectively.

Conclusion:

Credit can be both a lifeline for clients and a powerful growth tool for your veterinary practice— but only when managed wisely. Vet Mkononi makes it easy to track, manage, and control your clinic’s credit system without risking revenue or client trust.

By balancing compassion with sound business practices, Kenyan vets can build practices that are both profitable and sustainable for the long term.

Add a Comment

You must be logged in to post a comment